The SaaSPocalypse

One question that private investors and SaaS founders are asking a lot lately is “what’s going on with public SaaS stocks”?. The SaaSPocalypse, SaaSMageddon…no matter the clever label the decline in SaaS stocks has been dramatic. Why are people asking about this? Because public comps, while an imperfect valuation heuristic, are an important datapoint as it pertains to valuing private SaaS companies. But just as important as the valuation multiples are the underlying drivers for why SaaS is trading like it is.

So let’s dive in…

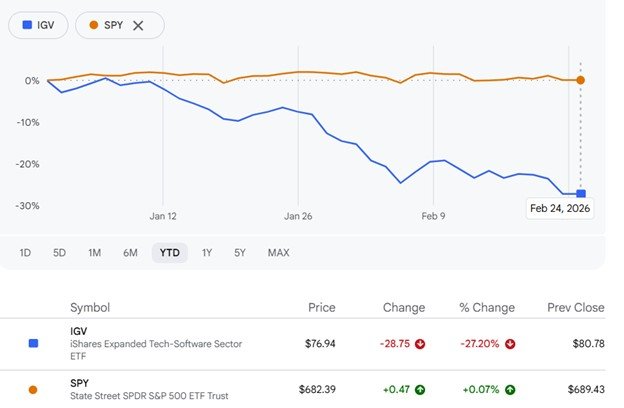

Public SaaS Performance vs. the S&P 500

The IGV index’s (the vast majority of which is comprised of public SaaS) performance vs. the S&P 500 this year has been downright awful…

2026 YTD: IGV vs. SPY

Source: Yahoo Finance as of Feb 23, 2026

Unsurprisingly the poor performance of SaaS stocks has dramatically derated their multiples with the median public SaaS stock trading at ~4x next twelve months revenue. That said, the following from Jamin Ball at Altimeter is illuminating:

“However, the “narrative violation” metric here is the growth adjusted revenue multiple median is still 0.35x vs the pre covid average of 0.28x (you can see the graph below, I post it every week). So while multiples are at historical lows, so are growth rates.”

Source: Clouded Judgement 1.30.26 - Software is Dead...Again!

So while it might be true the revenue multiples look low they don’t necessarily look low once growth is factored in. Now that we’ve gotten the obvious out of the way – SaaS stocks are indeed struggling mightily vs. the broader market and have rerated to a much lower multiple than in recent years let’s dive into what we think the primary drivers are…

The Commodification of Code

The rise of “vibe coding” generally has generated massive fear among investors that coding SaaS is going to become incredibly commoditized. What is “vibe coding”? Essentially it’s an AI-assisted software development approach that leverages LLM models such as Claude, where the user guides the creation of applications through natural language prompts rather than arduously writing manual syntax. Why does this commodification of code scare investors? Because it implies that the barrier to entry to launching a SaaS application is going to fall precipitously thereby leading to a massive influx of market supply. Vastly increasing SaaS supply = vastly decreasing pricing power plus much higher customer acquisitions costs as new competition floods the market. Investors fear not only competition from new vibe-coded SaaS entrants but potentially from corporates themselves who will opt to code their own applications vs. buying from a vendor. Why pay for a CRM tool if I can use Claude to create my own?

Agentic AI Commoditizing Legacy SaaS Licenses

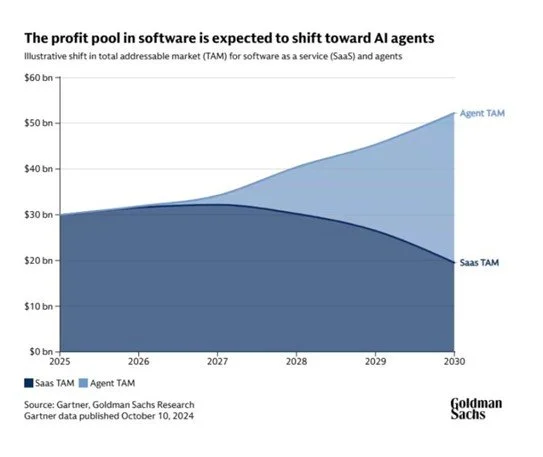

Investors are also fearful that IT spend generally is going to shift away from legacy SaaS towards agentic AI – even if one assumes that corporates may not cut IT spend in favor of vibe-coding their own solutions there is a fear that spend is going to migrate from traditional, seat-based SaaS towards agents and/or agentic AI native startups. Why continue to buy as many seat-based licenses from a legacy SaaS vendor if agentic AI automates the work? Think about something like an AR-automation software business – if autonomous agents are taking automatic action on behalf of collection reps (i.e. sending dunning notices) do you still need as many licenses for the AR-automation software? In sum, the more efficient your agentic AI is the less SaaS you need to buy. Goldman Sachs put out a chart recently that illustrates this potential phenomenon:

Source: Goldman Sachs Research

LLMs Enter the Application Layer

OpenAI and Claude are aggressively moving down the technology stack, evolving from primarily infrastructure providers to a direct competitor to legacy SaaS.

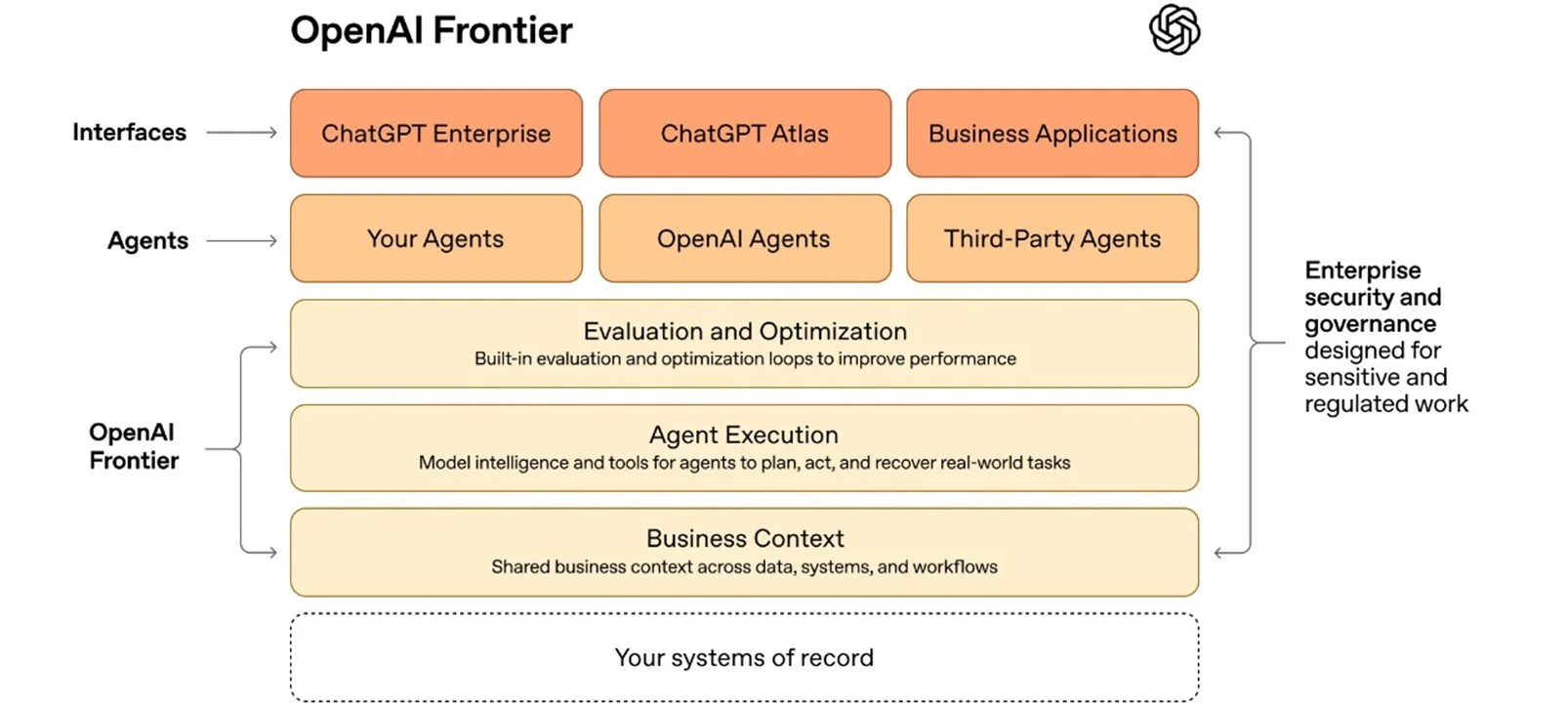

Indeed, earlier this year OpenAI launched its most direct assault on legacy SaaS with OpenAI Frontier. Frontier is a full-stack workflow orchestration layer engineered to build and deploy autonomous agents that can navigate existing software UI, supervise databases, and effectuate multi-step business logic sans human intervention. The market interpreted Frontier’s launch as OpenAI evolving from a tool that augments traditional SaaS to something that aims to replace SaaS itself. Just take a look at this diagram that OpenAI released:

Source: OpenAI

If legacy SaaS end up at the bottom of the OpenAI Frontier stack as easily digested systems of record with low switching friction what happens to the economics? Investors decided nothing good.

And to add to the concern on February 23rd Open AI announced “Frontier Alliances” whereby OpenAI is partnering with consulting firms like McKinsey, BCG, and Accenture to create a direct-to-enterprise pipeline that bypasses traditional software vendors in favor of deploying OpenAI agents.

Anthropic is getting into the game too – on February 20th Claude released a cybersecurity product – Claude Code Security which scans codebases for security vulnerabilities and suggests targeted software patches for human review. Cybersecurity SaaS stocks promptly plunged with Crowdstrike down ~20% in the subsequent two trading days.

Where’s the Cash Flow?

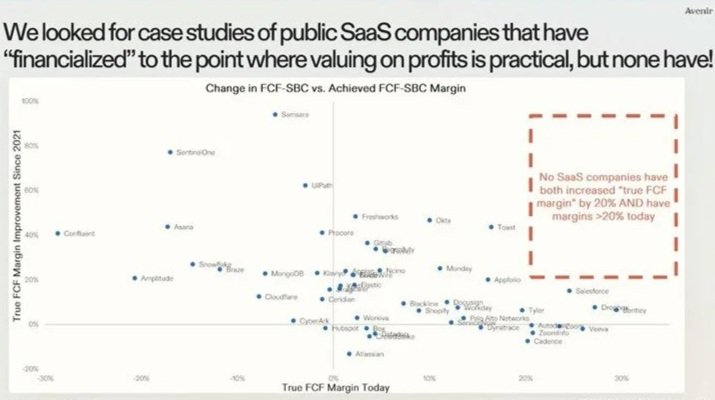

The investment thesis for SaaS has historically relied on the J-curve theory – essentially that in the early days SaaS is usually unprofitable (nadir of the J) as investment in product, go-to-market precedes the realization of operating leverage and, in turn, cash flow as a company matures (upward slope of the J). Public SaaS companies, however, even after the halcyon growth during COVID are still struggling to realize significant profitability at scale which is calling into question the ability for legacy SaaS to generate meaningful cash flow at maturity. The chart below from Avenir Growth does a terrific job of summarizing the problem – since 2021 zero public SaaS companies have both increased FCF margin (importantly this does not exclude SBC as this is a real cost borne by shareholders) by 20%+ while simultaneously achieving 20%+ margins. In fact, only a handful have 20%+ margins at all, which is concerning given how much incremental ARR was captured in the last five years. To make matters worse without FCF there isn’t much valuation support if investors decide software is a maturing industry and rerate away from revenue multiples towards PE / FCF multiples.

Source: Avenir Growth

Theories abound for why public SaaS has struggled to generate meaningful cash flow…some investors think it’s a secular issue driven by massive private sector investment into SaaS fueling ever increasing competition (leading to inflated sales and marketing expenses and capped pricing power), others believe culturally and philosophically these companies were built for a “ZIRP” environment when cheap debt and perpetually rising stock prices fueled poor operational discipline. Either way public market investors are getting impatient, especially given the other existential risks described that call into question future cash flows informing DCF valuations. Not only that, but investors are concerned that the expensive compute associated with launching generative AI products to thwart competition from AI-native upstarts represents another headwind against expanding cash flow margins.

So, Now What?

As an early-stage private SaaS company it doesn’t make sense to stress over where public SaaS is trading but the catalyzing concerns for lower public SaaS stock prices are beginning to cloud the private markets as well. So, it makes sense to stay apprised of the dynamics and know how to position against them. A few thoughts on how to do so…

Are You Truly a System of Record with High-Switching Costs

Investors in the current environment are tending to shy away from horizontal, workflow orchestration SaaS in favor of verticalized “system of record” platforms with high-switching costs (e.g. entrenched into multiple workflows / synthesizing data across multiple departments / continual API updates) and proprietary datasets that can be capitalized on with AI. The more you can position towards the latter vs. the former the better.

Is Your Go-to-Market / Distribution Model Difficult to Replicate?

One massive advantage that some SaaS companies have over new entrants is their institutional knowledge on how to best market and sell software. It’s one thing to “vibe code” a new product it’s an entirely different thing to sell that product at low cost of acquisition across a variety of channels. Traditionally investors have seen a complex go-to-market motion as a bit of a disadvantage due to questions on scalability but perhaps that could be positioned as an effective moat now instead.

Do Your Unit Economics Indicate Forthcoming Operating Leverage?

The “growth at all costs” paradigm has fully transitioned to “(eventual) cash is king”. How do investors discern future operating leverage and cash flow? Unit economics. Retention metrics in particular are under greater scrutiny than ever before. Sophisticated cohort analysis has never been more important to optimize.

Do You Have an AI Upsell Strategy?

You might not be implementing AI today but you definitely need it on the product roadmap. If you don’t, if nothing else, you’re conveying to investors you don’t know how to read the room. How can you potentially layer on agentic AI to guard against seat-based pricing risk? Is your pricing model outcomes based vs. seat-based? Do you have a proprietary dataset that can be capitalized on with LLM?

Does Your Projected Cost Structure Align with Your AI Strategy?

Generative AI compute remains very expensive. Not to mention that launching new sophisticated AI products will probably require more time investment from customer support reps to ensure successful upsell. Are there other line items in your cost structure that you can reduce to compensate? Investors will want to know you’ve thought through not only the revenue upsell associated with AI but the incremental costs as well.